Patent-Based Tax Savings in Korea: A Strategic Guide for Businesses

Pine IP Firm

November 29, 2024

Are you looking for ways to reduce your tax burden while leveraging intellectual property assets? Patents can serve as a powerful solution for both corporations and individual business owners in Korea. Through well-structured strategies, you can lower your corporate and personal income tax at the same time. Below, we explore how to utilize patents for tax efficiency using a sample patent valued at 300 million KRW (approximately 3억 원) and highlight key points to consider along the way.

1. Transferring a Patent Owned by the Representative for Personal Income Tax Savings

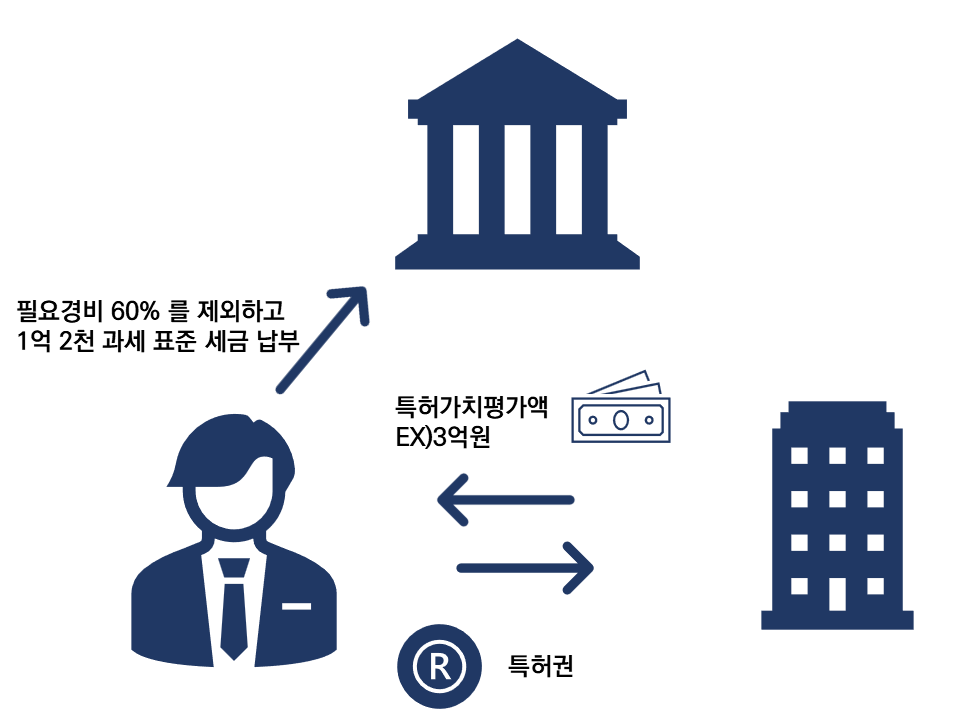

When a company’s representative (or owner) transfers a personally held patent to the corporation, the proceeds are treated as “other income” (기타소득). The main advantage of classifying income as 기타소득 is the 60% deduction for necessary expenses, which can result in a lower effective tax rate compared to salary or dividends.

1.1. Example: Comparing Different Tax Scenarios

Scenario 1: Annual Labor (Salary) Income of 500 million KRW

Taxable base: Approximately 478.9 million KRW (after earned income deductions)

Estimated total income tax (including local tax): about 165.82 million KRW

Scenario 2: Annual Labor (Salary) Income of 200 million KRW + Patent Transfer of 300 million KRW

Patent-related income: 300 million KRW with a 60% expense deduction (180 million KRW) leaves 120 million KRW as taxable.

Combined taxable base: 184.25 million KRW (labor income) + 120 million KRW (other income) = 304.25 million KRW

Estimated total income tax (including local tax): about 105.93 million KRW

Tax Savings vs. Scenario 1: Approximately 59.9 million KRW

By transferring the patent to the corporation, the representative can reduce personal tax by nearly 60 million KRW compared to earning the same amount solely as salary.

2. Using Patent Transfers to Resolve “Ga-ji-geum” (가지급금)

In Korea, “ga-ji-geum” refers to funds taken from the company without proper documentation or clear business purpose. Such transactions often cause higher tax liabilities for both the company and its representative:

Increased Corporate Tax: Unresolved ga-ji-geum is subject to a notional annual interest rate (4.6%), treated as non-operating income for the company, leading to higher corporate taxes.

Additional Personal Income Tax: The interest portion can be reclassified as a benefit or “deemed dividend” to the representative, resulting in extra personal tax obligations.

2.1. Example of Ga-ji-geum Over Five Years

If a company fails to clear 300 million KRW of ga-ji-geum for five years, it can incur a total tax burden of roughly 68.19 million KRW.

The longer ga-ji-geum remains unresolved, the more taxes and penalties add up.

2.2. Offsetting Patent Transfer Income with Ga-ji-geum

When the representative transfers a patent valued at 300 million KRW to the corporation and offsets (or “nets”) the transfer proceeds against the ga-ji-geum, the following benefits emerge:

Corporate Tax Savings: No further notional interest is accrued on the resolved ga-ji-geum.

Personal Income Tax Reduction: The patent-transfer income is eligible for a 60% expense deduction under 기타소득, lowering the effective tax rate compared to regular salary.

If the representative were to repay the full 300 million KRW ga-ji-geum through salary alone, they’d be taxed on the entire amount as wage income. However, by transferring a patent (which has a 60% deduction for necessary expenses), only 120 million KRW (40% of 300 million KRW) becomes taxable for personal income tax, significantly reducing the tax burden.

3. Corporate Tax Benefits through Patent Depreciation

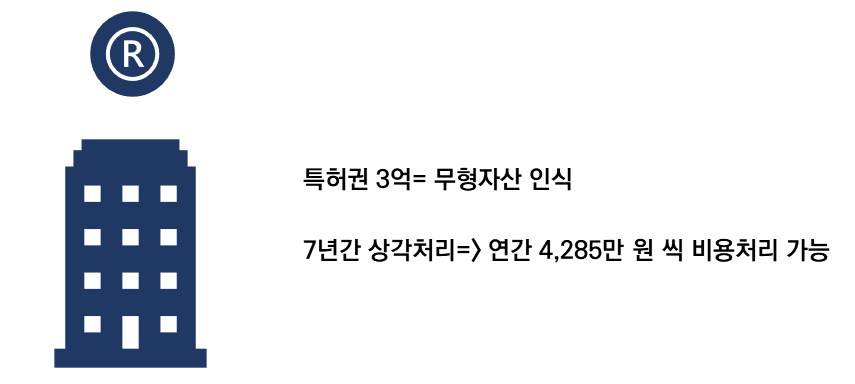

Once the company acquires the patent, it can record the patent as an intangible asset on its balance sheet. Under Korean tax law, the company can then amortize the patent’s value over seven years, reducing its taxable income each year.

3.1. Depreciation Example: Patent Valued at 300 Million KRW

Acquisition Cost: 300 million KRW

Annual Amortization: 300 million ÷ 7 years = ~42.85 million KRW per year

Annual Corporate Tax Savings (assuming a 22% corporate tax rate): ~9.43 million KRW per year

Cumulative Savings Over Seven Years: ~66 million KRW in reduced corporate tax

4. Key Considerations for Effective Patent Tax Planning

Fair Patent Valuation

Overstating or understating the patent’s value can trigger tax authorities to reject the transaction as a “sham.”

It’s critical to obtain an objective patent valuation report from a recognized valuation firm.

Clear Cost-Bearing Records

The representative must have personally funded the patent’s R&D or filing costs.

If corporate funds were used to develop or acquire the patent, ownership belongs to the company, making the personal transfer strategy invalid.

Overall Benefits for the Representative

Reduced Personal Tax through the 60% expense deduction on 기타소득

Resolution of Ga-ji-geum issues without incurring extra taxes on wages or dividends

Overall Benefits for the Corporation

Corporate Tax Savings through intangible asset amortization

Stronger Balance Sheet by capitalizing the patent as an intangible asset

5. Maximizing Your Patent-Based Tax Strategy

Patent-based tax planning can significantly benefit both the individual representative and the company. However, achieving optimal outcomes requires meticulous planning, proper valuation, and expert execution. Pine IP Firm can help you:

Obtain an accurate patent valuation

Design a comprehensive tax-saving strategy

Coordinate the ga-ji-geum resolution and manage amortization schedules

With the right approach, you can minimize taxes, improve cash flow, and strengthen your company’s financial position—all while making the most of your intellectual property assets. Contact us today for a professional consultation, and discover a tailored solution that works for both you and your business.